What's the best way to distribute money in retirement?

The most commonly cited rule for making distributions in retirement is wrong. Most people hear it's best to first fully distribute your taxable account balances, then your tax deferred account balances, and finally your tax free account balances. This reduces the value of your deductions. More valuable alternatives include first filling up your deductions with pre-tax distributions.

What's the best way to distribute money in retirement? Most people assume (and a lot financial planning software suggests) that distributing your taxable accounts first, then your tax deferred accounts, then your tax free accounts last is the way to go.

This is a type of distribution “waterfall” where you only focus on distributing one type of account at a time. You’re only distributing taxable until you’ve used all those dollars, then you shift your attention to pre-tax accounts, and finally tax free accounts.

But you can do better than this. Let’s look at two scenarios.

Let's say you and your spouse are 65. You're retired. You need $100k in distributions. You haven't started Social Security yet. You have a $500,000 taxable brokerage account and a $1,000,000 pre-tax IRA. For simplicity we will assume they both grow at 7% and inflation is 3%.

Your standard deduction is going to be $35,500. On top of that you get a $12,000 bonus deduction (this goes away after 2028).

Let's say you have a 50% gain in your taxable brokerage account. This means if you need $100k you'll realize $50k in gains on a $100k distribution.

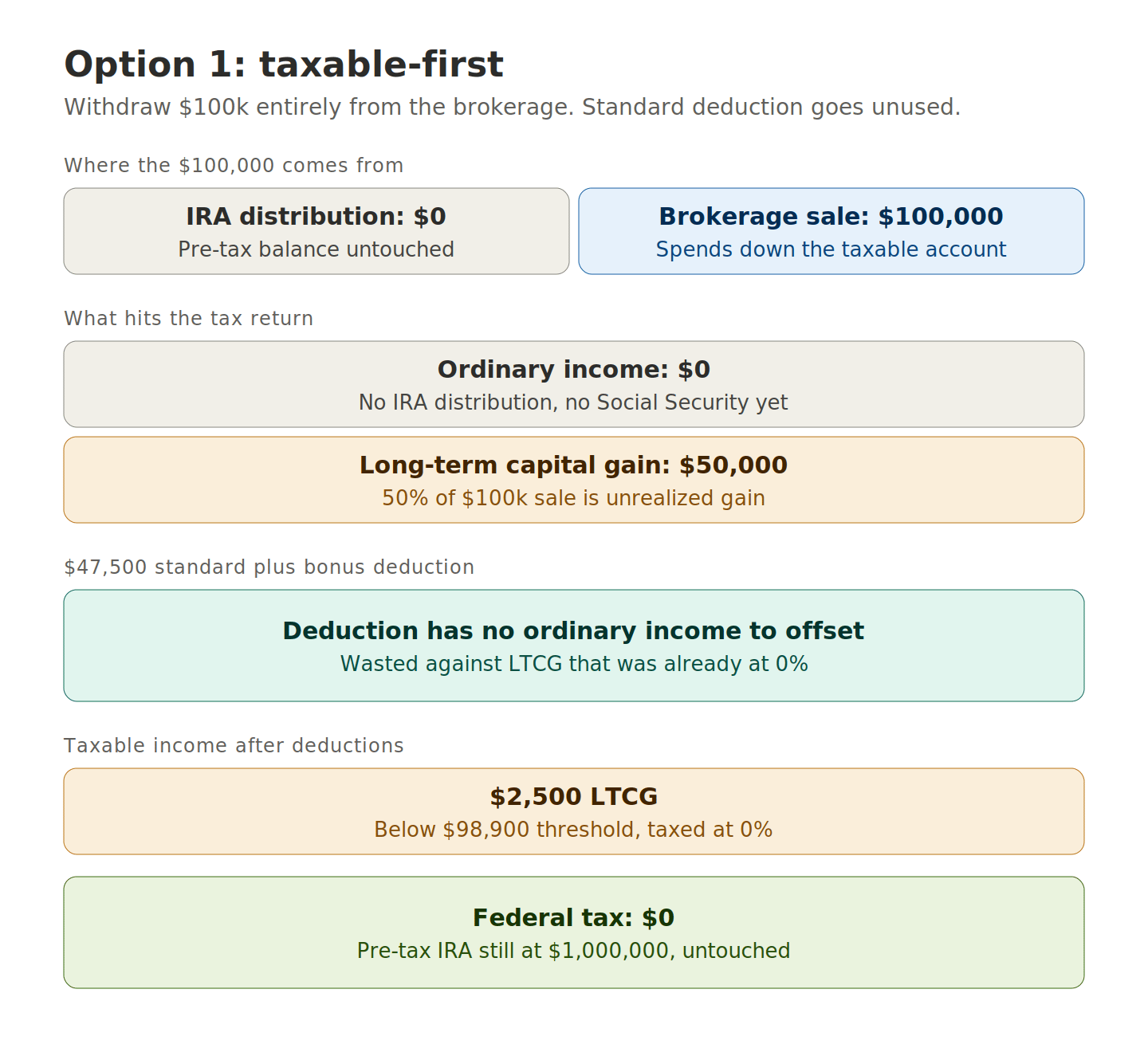

Option 1: Taxable, Tax-Deferred, Tax-Free

If you decided to follow the standard rule you'd distribute $100k, have $50k of AGI. You'd get $35,500 + $12,000 in deductions. Your taxable income would be $2,500.

Since you pay a 0% capital gains rate on taxable income below $98,900, you owe $0 in tax. Your pre-tax IRA is left untouched.

By age 71, when you are claiming Social Security, your taxable brokerage is about to be exhausted and you switch over to pre-tax distributions.

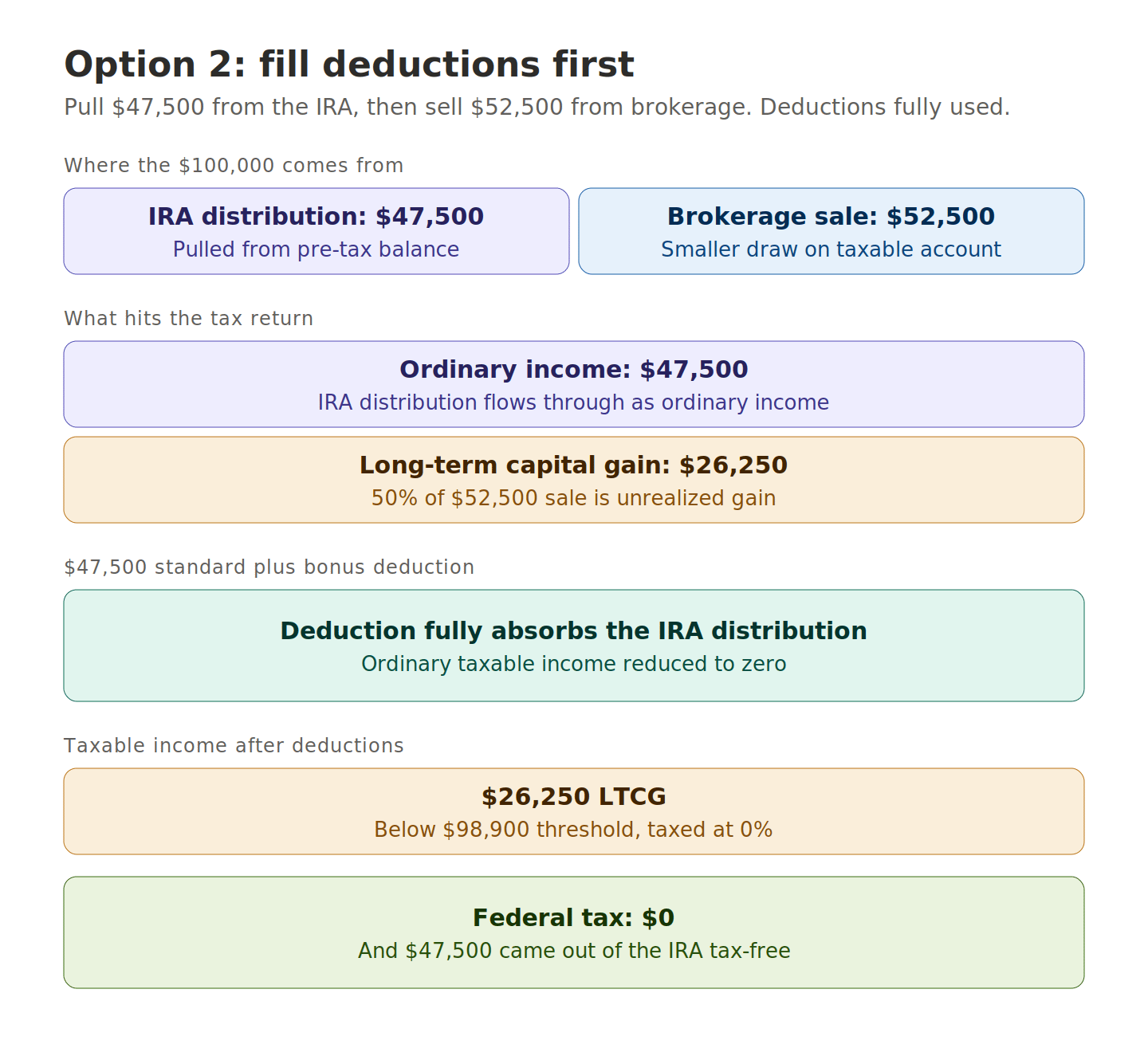

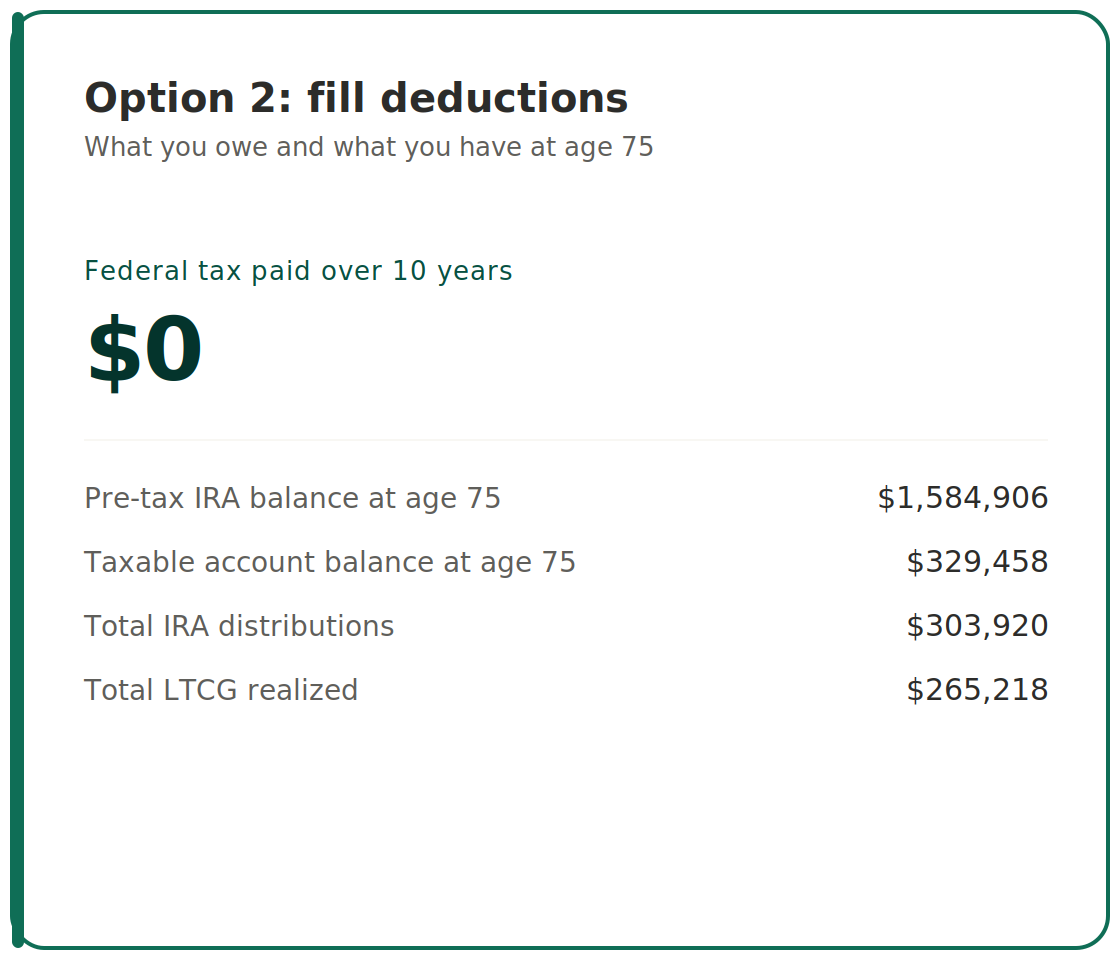

Option 2: Take advantage of your deductions

Instead of this, you could instead make a $47,500 distribution from your pre-tax IRA. You still need $100k - $47,500 = $52,500k, so you realize $52,500*50% = $26,250 in long term capital gains to get you to $100k in distributions.

Your deductions will completely wipe out the $47,500 IRA distribution. You'll then have $26,250 in taxable income. But since you're still in the 0% long term capital gains tax bracket, you won't owe any tax on them.

You’ve achieved the same thing as in the first scenario where you followed the standard rule, distributing your taxable account first but you have the added benefit of reducing your pre-tax account balances with out paying any taxes.

When you flip on Social Security at age 70 in this scenario, your IRA distributions drop by quite a bit because your taxable Social Security is consuming a portion of your standard deduction. But you have more of your taxable brokerage account to draw on.

The Payoff

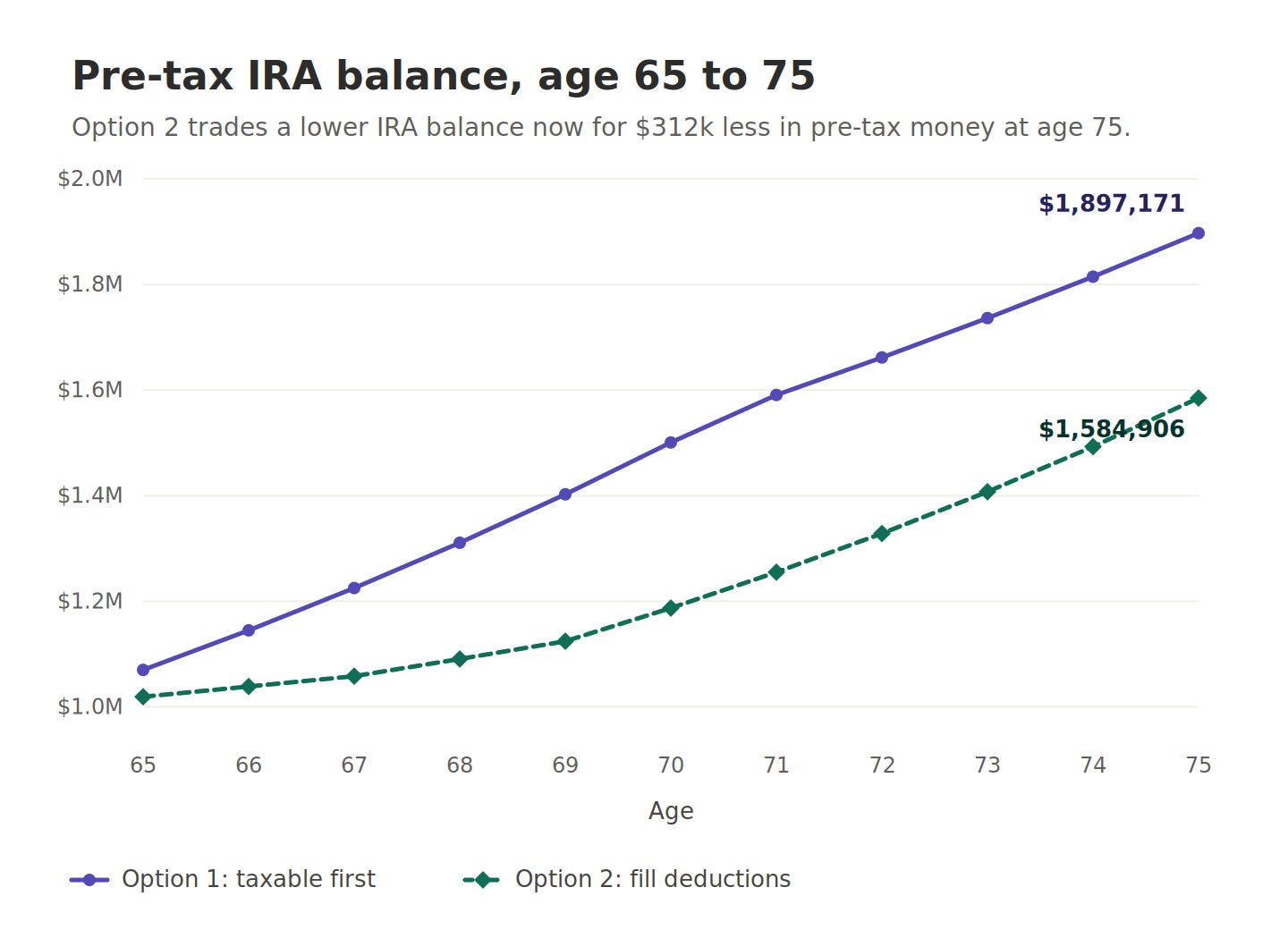

The big payoff comes when Social Security and RMDs kick in and you're forced to distribute those pre-tax balances. You won't be able to take advantage of a 0% tax rate at that point.

Let’s say you continue with this distributions in option 2, your pre-tax account balance at your RMD age (75) will be about $300,000 less than your pre-tax account balance with option 1. That’s because you were able to take about $131,000 more in distributions from your IRA (without paying any taxes!) from you pre-tax accounts under option 2.

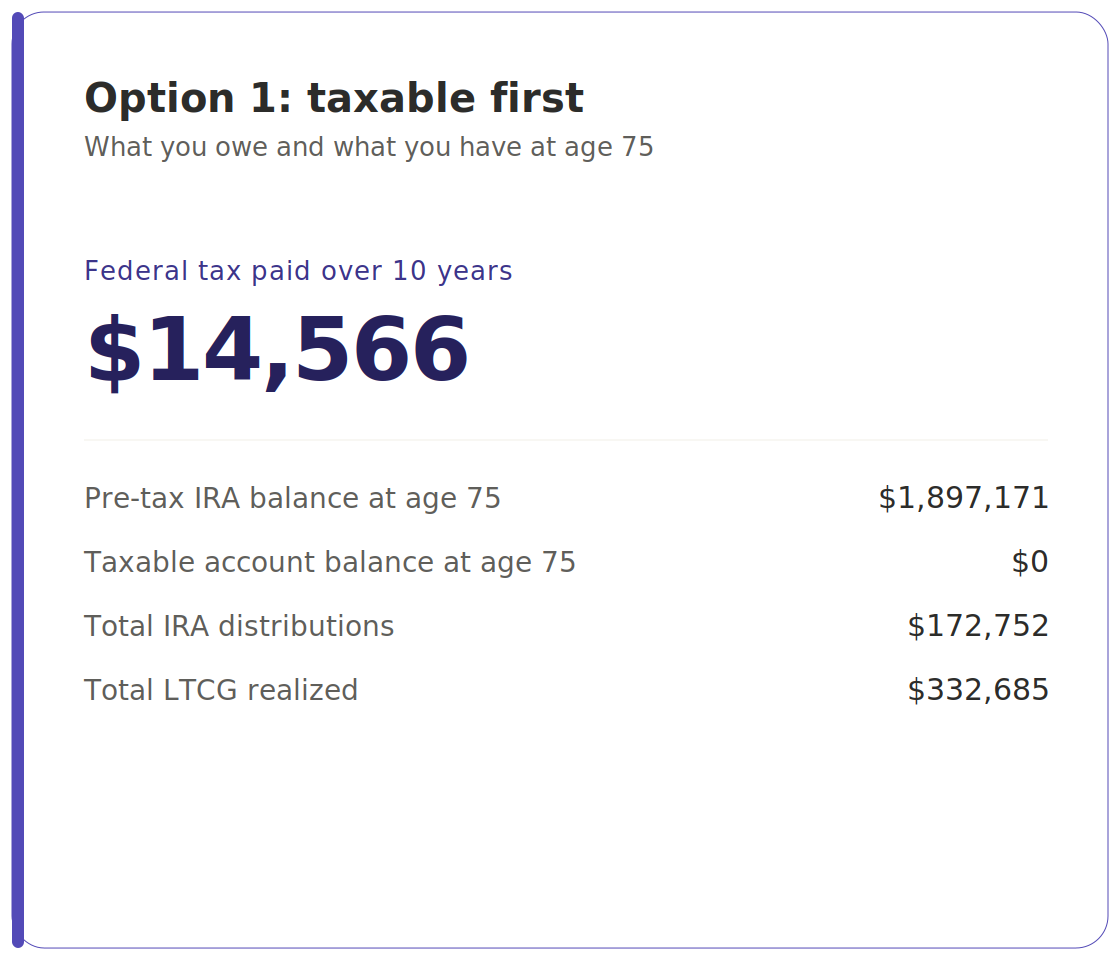

Under current law you first year RMDs under option 2 would be about $11,800 less than under option 1. If we assume a 22% marginal federal income tax rate that’s about $2,600 in extra tax the year RMDs kick in.

Ultimately, after 10 years, in option 1 you would have cumulatively paid about $14,500 in federal income taxes and under under option 2 you wouldn’t have paid a single dollar in federal income taxes.

The takeaway here is to not waste your standard deductions (or special bonus deduction) on long term capital gains.

Have questions about your retirement plan?

Schedule a free, no-pressure introductory call with Erik.

Schedule a Call